2. Excerpts from Slide Show Presentation

|

|

Today’s Announcements LINT Creating Liberty Digital Commerce tracking stock group: Tickers: LDCA and LDCB Renaming remaining Liberty Interactive Group to QVC Group New tickers: QVCA and QVCB |

Filed by Liberty Interactive Corporation pursuant to Rule 425 under the

Securities Act of 1933 and deemed filed pursuant to Rule 14a-6(b) of the

Securities Exchange Act of 1934

Subject Company: Liberty Interactive Corporation

Commission File No.: 001-33982

Excerpts from the Transcript and Slide Show Presentation of the

Liberty Interactive Corporation Investor Day held on October 10, 2013

1. Excerpts from Transcript

Gregory B. Maffei, President, Chief Executive Officer

. . . We are . . . happy to announce that we’re creating a couple of new [stocks] today. First, Liberty Digital Commerce, we’ve been working hard on an acronym — LibDig; didn’t go over as big as some would think, but I kind of like it. LDC; we’ll figure it out.

But we’re excited about announcing that today. Really two parts; first, creating a separate tracker out of Liberty Digital, and as a part of that, renaming QVC as its own tracker with the HSN interest, and then it’s out on the tickers QVCA and QVCB.

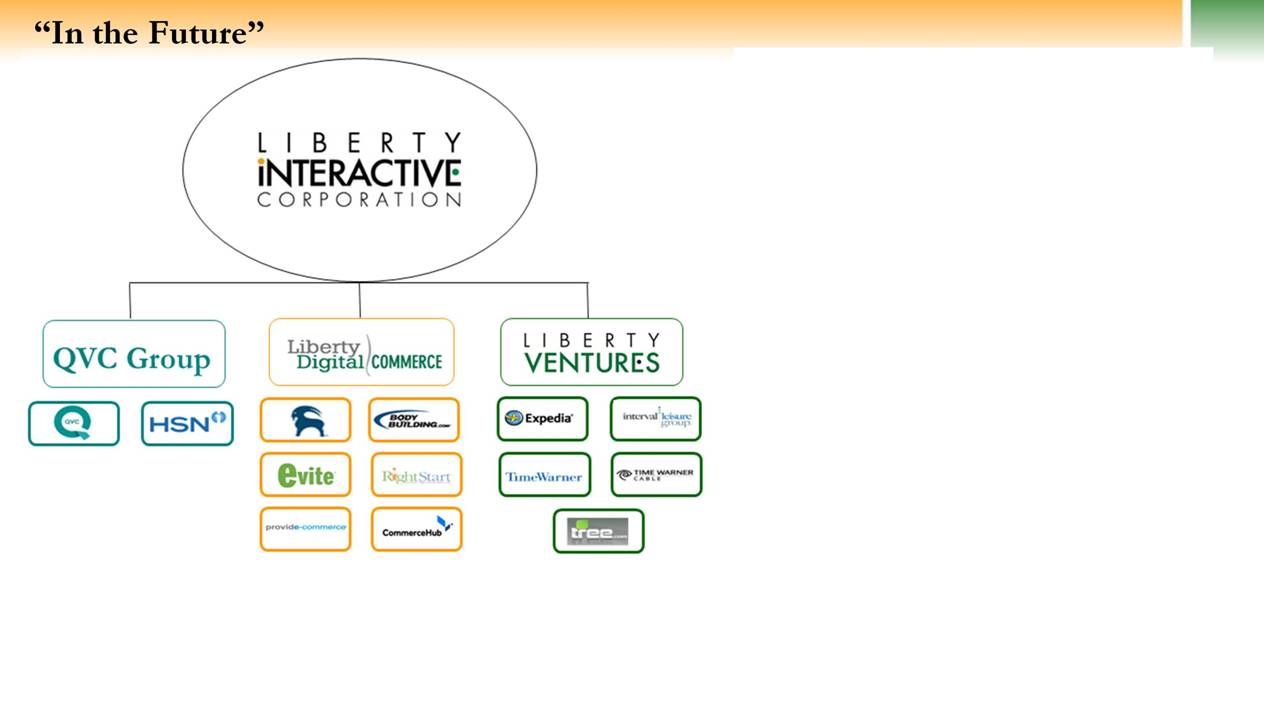

. . . So if you look at the structure today, Liberty Interactive has two trackers; LINTA and LVNTA. And as we go forward, [we will have] three trackers.

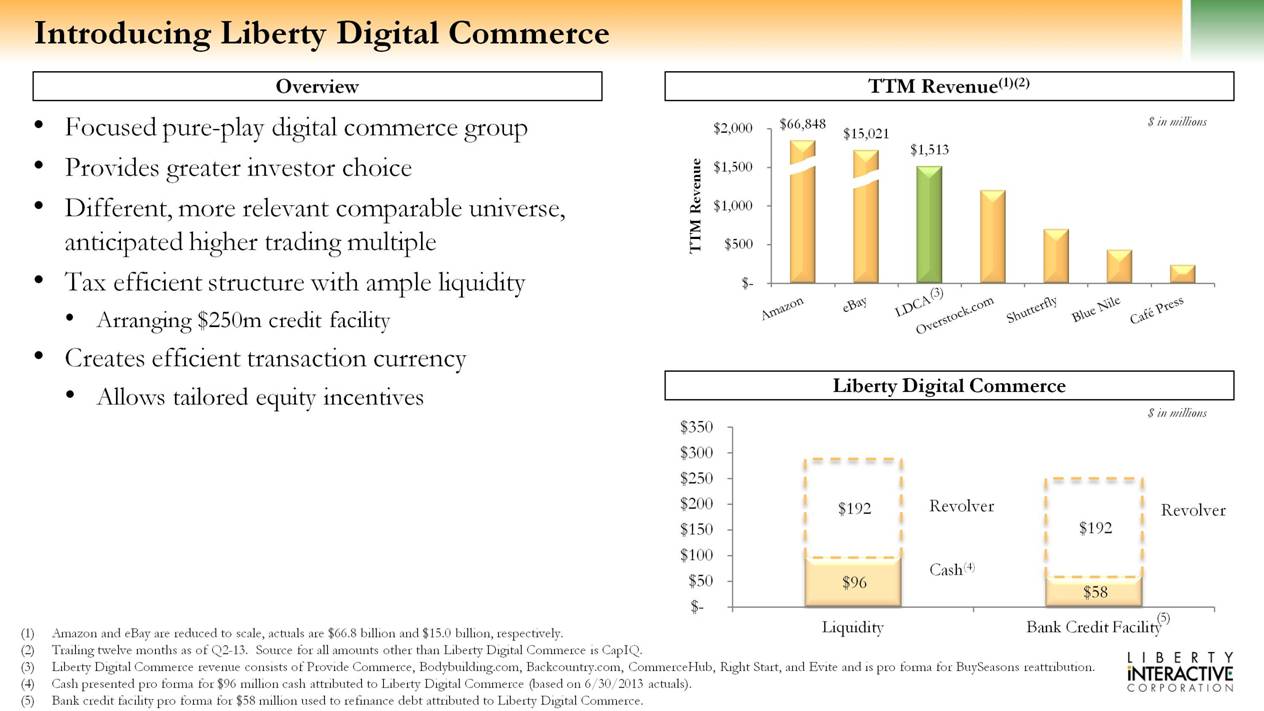

. . . So why are we doing this and what do we hope to achieve? First, by putting LibDig; Liberty Digital Commerce as its own separate [tracking stock], I think we’re going to have a more focused pure-play Digital Commerce Group. We’re going to provide choice to you. Some of you may prefer to be deeper in QVC. Some of you may prefer to be deeper in Liberty Digital Commerce.

If you look at the peer group, and we’ll talk a little about that; they tend to trade at a different multiple. These e-commerce companies, because of their growth, tend to trade higher. And if you look inside of the current LINTA structure, given the scale and size of QVC and some of the interest, but particularly with QVC’s EBITDA approaching $2 billion and their EBITDA closer to 100 plus, it was barely noticed. So to have them a chance to be recognized, called out, provide a tax-efficient structure, provide a currency, provide a way to have them have their own identity, we perceive that to be a positive.

Now, as a part of this, we are going to go out and arrange separate financing on that group. They currently maintain a credit balance to our facilities or against Liberty usually. It runs about just under $60 million. In peaks, as they increase inventory, some of them do that. And as they had in the Q4 sales, others — like Backcountry, others then do it earlier. For example, BuyCostumes put their inventory out as they head towards the Halloween season, and if you looked at ProFlowers, it probably peaks its inventory as it heads into Valentine’s Day and Mother’s Day.

So they all have different cycles for what their usage of capital is. But if you take the average across the year, it’s running about a $60 million balance, just under, and we’re going to have about a $250 million facility; so ample credit — ample liquidity going forward. Those slides on the right show that it’ll be a large among focused e-commerce companies. There are two giants. But after that, it’s a very large company for that nature. And this slide at the bottom shows liquidity, both coming from incremental revolver, available revolver, and cash that’s there.

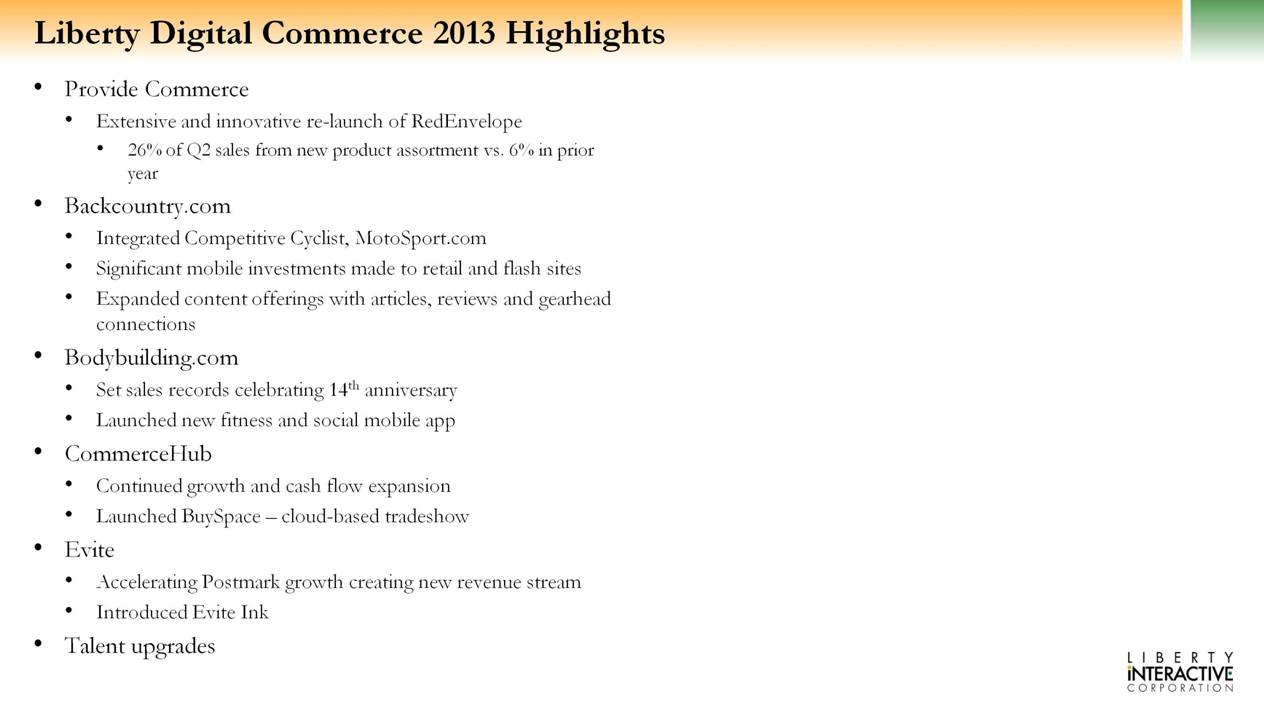

Some of the highlights of these businesses in 2013 included Provide. They did a very innovative re-launch of RedEnvelope; Chris Shimojima will talk a lot about that in a bit. But a substantial portion of its sales are now coming from a new product assortment. At Backcountry, they integrated [Competitive Cyclist], which they’ve bought the prior year, and MotoSport, which we bought this year; both important assets to broaden their appeal to consumers.

And to some degree, to make them less exposed to weather. Neither of those are on the same cycle as many of the outdoor winter products, that Backcountry sells, like skis, snowboards, et cetera. They also made significant mobile investments, upgrading both the retail and flash sites. And they expanded their content offering, increasing their appeal, both on — for natural search.

Bodybuilding had a great uptick in sales. On their 14th anniversary in particular, they’ve set enormous daily sales records. But across the year, if you look at how they’ve excelled at revenue growth; very impressive. They also launched a new fitness and social mobile app that leverages their body space content, and the workout regimes they have. And I think — I encourage you to download it.

CommerceHub, which we’ve spent less time talking about. It’s more of a B2B business than a B2C business like there are others of our e-commerce companies. CommerceHub has continued to have a great growth, and expand its margins and expand its cash flow. They also launched BuySpace, which effectively is a way for them of vendors to come and post products on BuySpace and have retailers search for them, and make connections through CommerceHub, through the drop-ship capabilities of CommerceHub that’ll greatly expand their inventory.

So if they have traffic, if they have mobile, and if they have e-commerce traffic but they don’t want to carry the inventory, they don’t necessarily have ability to handle all of those products, they can make that connection through BuySpace, and have vendors supply that. We are very excited about that. And as I said, it’s not a B2C product, but it really does enable B2C offerings for others.

And lastly, at Evite, among the companies, we saw Postmark, which is their paid rather than advertiser-supported invite model grow, and we saw them introduce Evite, Inc., which is basically an opportunity to send Evites and other kinds of collateral through the mail on a physical good.

Lastly, I think, if you look across the whole Group, we really have been upgrading talent. At Provide Commerce, we have a new CEO; Chris Shimojima has been there about a year and a half; a little more. Backcountry added a new COO. . . .You’re going to hear from Dev, who’s been with us now about eight months or nine months. CommerceHub; Frank Poore, who had founded it and left, came back about a year, year and a half ago. And across the Group, we really see incremental talent and a continued focus on more professional management.

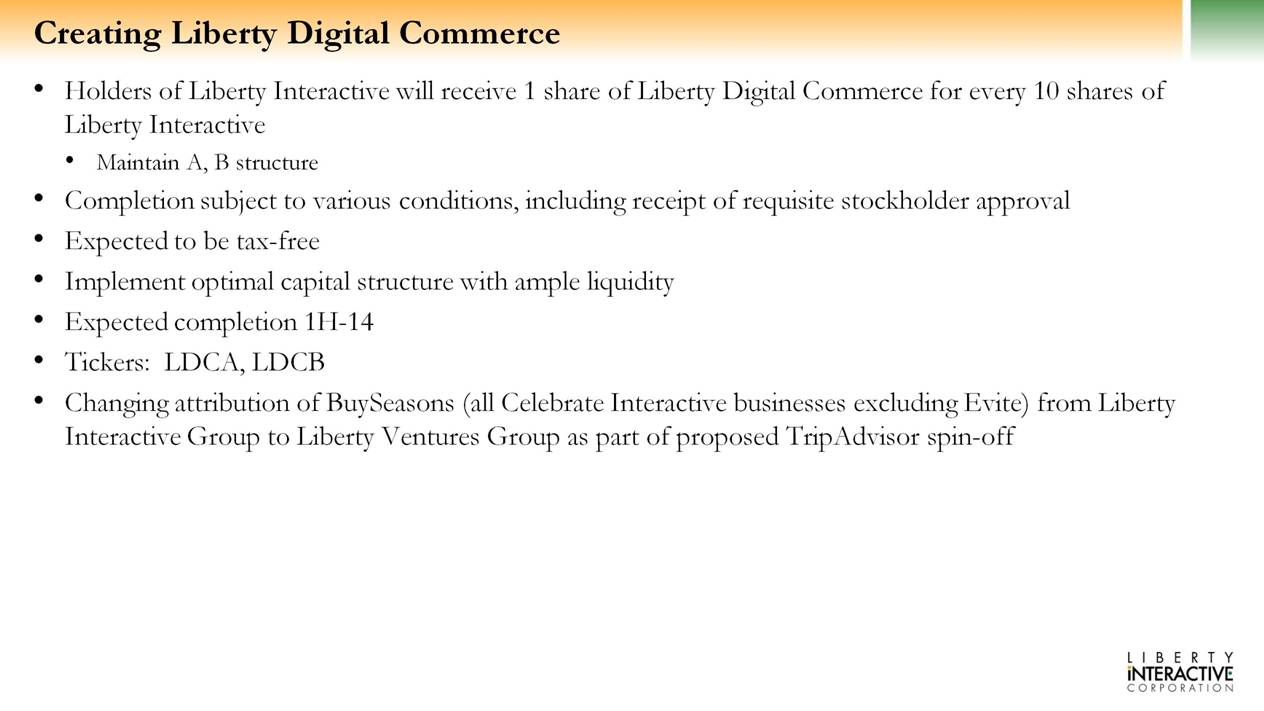

So what will actually happen as we create Liberty Digital Commerce? Holders of LINTA will receive one share of Liberty Digital Commerce for every 10 shares of LINTA. We’ll maintain our A, B structure, charter and bylaws. All the other corporate governance issues will largely be the same. Obviously, we’ll not have a separate Board as it fits into the tracker inside of Liberty Interactive. There are some conditions, including a receipt of shareholder approval. We expect it to be tax-free. We are, as I said, putting in a credit facility we think will optimize its capital structure.

Hope to get it done, I’d like to say in Q1, but the lawyers make me say first half. And one thing to note is because of this process and the thing I’m going to talk about next in creating Trip Holdings, we’re going to move BuySeasons, which is currently attributed into LINTA and attributed over to Liberty Ventures, and then into Trip Holdings.

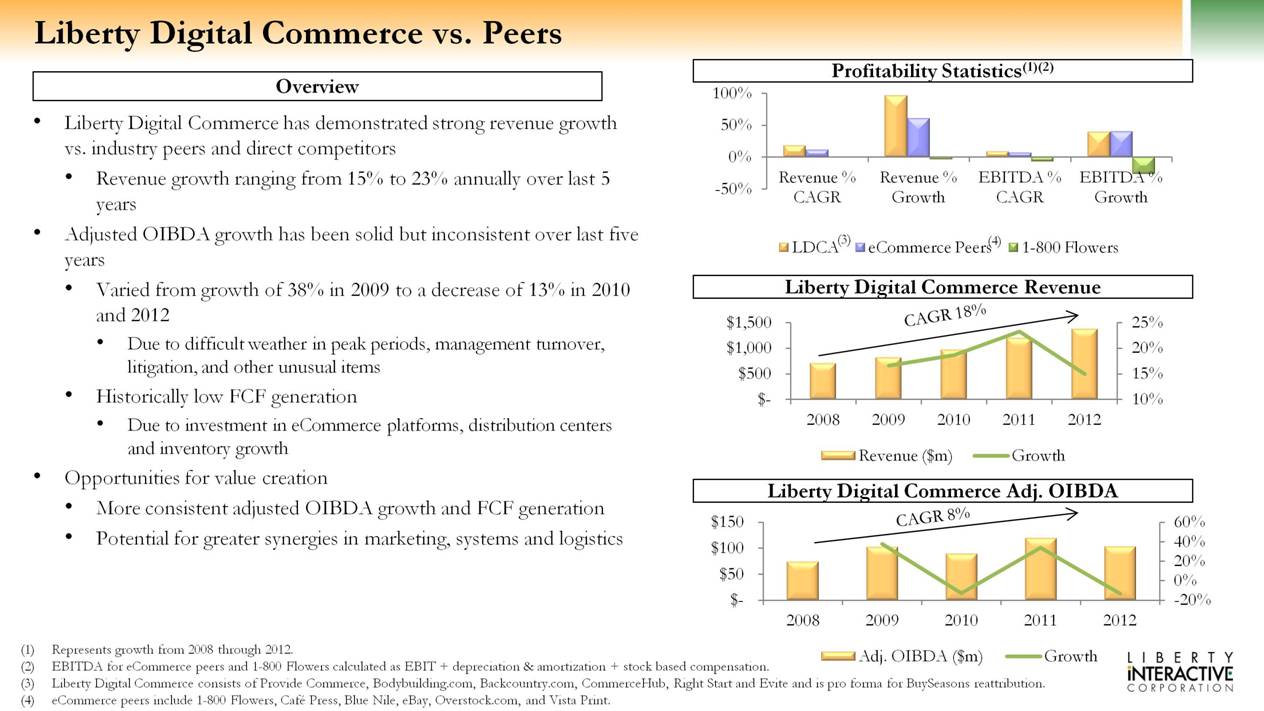

Now if you look at those Liberty Digital Commerce companies, and it is multiple companies, and compare them to their peers, if you take a longer term timeframe, they’ve exhibited growth well in excess of their peers. Now in the last 18 months, we’ve had some hiccups. But if you take a longer perspective, and even the more recent quarters, they’ve been well above the peer group average.

OIBDA growth has also been above the peer group average, with some hiccups in the last 18 months. And some of that has occurred in the last period due to bad weather. It’s not been a great winter for Backcountry, the last two. We’ve had some management turnover, some of it of our choosing. We’ve had some litigation, which had incurred expense, and some other one-time items we believe.

Historically, these businesses have had — not had the free cash flow generation that we have so savored and favored, but we are — we have seen investments we believe can lead to future growth. Some of those include the investments in e-commerce platforms. Some of that includes distribution centers and a new headquarter, for example, at Bodybuilding.com. And some of that has just been to fuel inventory. And certainly, our focus in

value creation going forward is to build a more congested — consistent adjusted OIBDA path and have higher free cash flow generation.

In addition, as we look out, we have not really treated these as one company. This has been run as a series of individual businesses. One of the reasons we attracted these businesses and these management teams was the autonomy we gave them. But increasingly, to be competitive, I think you’ll see us make and take actions to try and have them be sharing logistics, sharing best practices, sharing synergies, potentially in systems, potentially in marketing. So that’s some of the focus going forward. And our hope is; through some of those actions to get a more consistent pattern of revenue growth, more consistent pattern of OIBDA growth, and more consistent pattern of free cash flow.

So QVC, renamed from LINTA to QVC Group, I think it’ll take recognition of the fact which that QVC is the main driver of LINTA today. It will become its own focus company. Mike George will talk a lot more about some of the benefits of that, and some of the highlights that are down below. But to touch on some them for you; cleaner comparable analysis, it’s a more effective trend acquisition currency if we decide to use it, allowed for tailor equity incentives just around the QVC Group. We will not change QVC’s leverage. We will not change its debt or cash balances. There’ll be no transfer between the two trackers upon the creation.

Some of the highlights; obviously still have industry-leading margins, significant free cash flow generation. It is growing its e-commerce dramatically in all markets, both on desktops and on mobile and on tablets. And Mike George will talk about all those. One thing to note, obviously, is the mobile, up more than 75%, which is very impressive. And they begun, really to focus their social efforts. The most recent acknowledgement that is their launching of toGather, which Michael will also talk more about.

. . . So what are our priorities at this Group as we go forward? First, complete the tracker.

. . . At Liberty Digital Commerce, each of the companies probably has their own priority. First at Provide, re-energizing the repositioned RedEnvelope. At Backcountry, continuing to drive its authenticity to its customer set, the quality of experience, and the guidance that its Gearheads give its consumers are truly differentiating factors that they want to continue to push.

Bodybuilding.com has an enormous international opportunity. And its opportunity also to leverage its newly re-launched social mobile app, I think, is very interesting, and you’ll hear more from Ryan about that topic. At CommerceHub, I mentioned, BuySpace; absolute enormous opportunity for them. And in all these companies; we need to take advantage of the scale we have, which is quite large for an e-commerce group, and try and improve our free cash flow delivery, and maintain capital flexibility.

. . .

Question:

Can you talk about now that you have or you will have two stocks what the acquisition strategy will be for QVC and for the digital assets?

Answer: Gregory B. Maffei

Well, I think if you look QVC has done a few kind of fold-in technology-type, social-type acquisitions it’s in the trend in Oodle, both relatively small but fit their and added to their product portfolio or capabilities. And I guess it’s potentially the case with some of the e-commerce companies could find an asset that they wanted that would be similar and there are places where they rub up against each other. But in general, they have not done many acquisitions at QVC in the e-commerce type space, and the companies that we have added into the e-commerce group or the Liberty Digital Commerce group now has been ones that are more point nichey e-commerce plays and have not really been of interest to the type of companies that have been through to QVC. So, there is a potential to rub up against each other, but historically that really hasn’t happened.

. . .

Question: Trisha Dill, Analyst, Wells Fargo Securities LLC

Hi. Trisha Dill at Wells Fargo. Just a couple of questions on Liberty Digital. Do you plan to provide operating results by asset after the recapitalization? And then secondly, can you talk a little bit more about the potential

synergies that you hope to realize as you think about running the individual businesses more as one company? And what that might mean to EBITDA and free cash flow? Thanks.

Answer: Gregory B. Maffei

. . . [S]ome of the units are large enough that we’ll probably have to provide operating results on them.

. . . On the synergies side, there are some nascent things we’ve done around things like shipping contracts. We’ve attempted some things around healthcare. We are — have looked at some things around logistics. And you’re seeing nascent parts of that; things like Dev’s or Celebrate’s excess warehouse space being consumed and utilized by Bodybuilding.com.

But there’s more clearly we can do. We’ve done some interesting things around mobile in some of the companies. But I would say, largely in our companies, there’s more opportunity in mobile. And should we be doing more together around mobile and trying to grab mobile platforms?

There are some opportunities perhaps around greater logistics capacity. We have a tension — a healthy tension, and that these are entrepreneurially-driven businesses that feel they know their priority is important to get — meet their customer needs, and trying to meet the needs of the Group versus the needs of the individual company is a healthy tension. So we will work through those.

2. Excerpts from Slide Show Presentation

|

|

Today’s Announcements LINT Creating Liberty Digital Commerce tracking stock group: Tickers: LDCA and LDCB Renaming remaining Liberty Interactive Group to QVC Group New tickers: QVCA and QVCB |

|

|

“In the Future” Create new board for Liberty TripAdvisor Holdings Maintain 57% voting interest & 22% equity interest Maintain representation on TripAdvisor Board |

|

|

Overview TTM Revenue(1)(2) Liberty Digital Commerce Focused pure-play digital commerce group Provides greater investor choice Different, more relevant comparable universe, anticipated higher trading multiple Tax efficient structure with ample liquidity Arranging $250m credit facility Creates efficient transaction currency Allows tailored equity incentives Introducing Liberty Digital Commerce (3) Amazon and eBay are reduced to scale, actuals are $66.8 billion and $15.0 billion, respectively. Trailing twelve months as of Q2-13. Source for all amounts other than Liberty Digital Commerce is CapIQ. Liberty Digital Commerce revenue consists of Provide Commerce, Bodybuilding.com, Backcountry.com, CommerceHub, Right Start, and Evite and is pro forma for BuySeasons reattribution. Cash presented pro forma for $96 million cash attributed to Liberty Digital Commerce (based on 6/30/2013 actuals). Bank credit facility pro forma for $58 million used to refinance debt attributed to Liberty Digital Commerce. (5) Revolver Revolver $ in millions $ in millions Cash(4) |

|

|

Liberty Digital Commerce 2013 Highlights Provide Commerce Extensive and innovative re-launch of RedEnvelope 26% of Q2 sales from new product assortment vs. 6% in prior year Backcountry.com Integrated Competitive Cyclist, MotoSport.com Significant mobile investments made to retail and flash sites Expanded content offerings with articles, reviews and gearhead connections Bodybuilding.com Set sales records celebrating 14th anniversary Launched new fitness and social mobile app CommerceHub Continued growth and cash flow expansion Launched BuySpace – cloud-based tradeshow Evite Accelerating Postmark growth creating new revenue stream Introduced Evite Ink Talent upgrades |

|

|

Creating Liberty Digital Commerce Holders of Liberty Interactive will receive 1 share of Liberty Digital Commerce for every 10 shares of Liberty Interactive Maintain A, B structure Completion subject to various conditions, including receipt of requisite stockholder approval Expected to be tax-free Implement optimal capital structure with ample liquidity Expected completion 1H-14 Tickers: LDCA, LDCB Changing attribution of BuySeasons (all Celebrate Interactive businesses excluding Evite) from Liberty Interactive Group to Liberty Ventures Group as part of proposed TripAdvisor spin-off |

|

|

Overview Profitability Statistics(1)(2) Liberty Digital Commerce vs. Peers (3) (4) Represents growth from 2008 through 2012. EBITDA for eCommerce peers and 1-800 Flowers calculated as EBIT + depreciation & amortization + stock based compensation. Liberty Digital Commerce consists of Provide Commerce, Bodybuilding.com, Backcountry.com, CommerceHub, Right Start and Evite and is pro forma for BuySeasons reattribution. eCommerce peers include 1-800 Flowers, Café Press, Blue Nile, eBay, Overstock.com, and Vista Print. Liberty Digital Commerce has demonstrated strong revenue growth vs. industry peers and direct competitors Revenue growth ranging from 15% to 23% annually over last 5 years Adjusted OIBDA growth has been solid but inconsistent over last five years Varied from growth of 38% in 2009 to a decrease of 13% in 2010 and 2012 Due to difficult weather in peak periods, management turnover, litigation, and other unusual items Historically low FCF generation Due to investment in eCommerce platforms, distribution centers and inventory growth Opportunities for value creation More consistent adjusted OIBDA growth and FCF generation Potential for greater synergies in marketing, systems and logistics Liberty Digital Commerce Revenue Liberty Digital Commerce Adj. OIBDA CAGR 18% CAGR 8% |

|

|

The QVC Group Renaming Liberty Interactive Group “QVC Group” to reflect main operating asset Trading under new tickers: QVCA, QVCB Further focus on QVC’s strong operating metrics Enables more efficient, directed share repurchase Cleaner comparable analysis Provides investor choice Creates efficient transaction currency Allows tailored equity incentives New tracker has no change on QVC level leverage, debt and cash balances QVC highlights Industry-leading margins and significant FCF generation eCommerce – solid growth in all QVC markets Strong mobile growth – up more than 75%(1) Launch of toGather – innovative social platform to optimize the existing QVC community Trailing twelve months as of June 2013 vs. prior year. |

|

|

Priorities Complete Liberty Digital Commerce tracker QVC Enter new international market every two to three years Drive mobile penetration to 35% of global commerce by 2015 Increase US internet penetration to ~50% by end of 2014 Innovate in social, mobile Maintain target QVC level leverage Generate returns through levered equity repurchases Liberty Digital Commerce Provide Commerce – reposition and re-energize RedEnvelope Backcountry.com – drive authenticity, experience, and guidance for our customers Bodybuilding.com – improve international customer experience and create new social and mobile tools to help customers succeed CommerceHub – expand BuySpace Scale companies Enhance FCF delivery Maintain capital flexibility |

|

|

Reconciling Schedules Preliminary Note This presentation includes references to adjusted OIBDA, which is a non-GAAP financial measure, for each of Liberty Interactive Group, Liberty Digital Commerce Group, and QVC (and certain of its subsidiaries). Liberty Interactive defines adjusted OIBDA as revenue less cost of sales, operating expenses and selling, general and administrative expenses (excluding stock and other equity-based compensation) and excludes from that definition depreciation and amortization, restructuring and impairment charges and legal settlements that are included in the measurement of operating income pursuant to GAAP. Further, this presentation includes adjusted OIBDA margin, which is also a non-GAAP financial measure. Liberty Interactive defines adjusted OIBDA margin as adjusted OIBDA divided by revenue. In addition, Liberty defines free cash flow as cash flow from operations less capital expenditures. Liberty Interactive believes adjusted OIBDA is an important indicator of the operational strength and performance of its businesses, including the ability to service debt and fund capital expenditures. In addition, this measure allows management to view operating results and perform analytical comparisons and benchmarking between businesses and identify strategies to improve performance. Because adjusted OIBDA is used as a measure of operating performance, Liberty Interactive views operating income as the most directly comparable GAAP measure. Adjusted OIBDA is not meant to replace or supersede operating income or any other GAAP measure, but rather to supplement such GAAP measures in order to present investors with the same information that Liberty Interactive’s management considers in assessing the results of operations and performance of its assets. Please see the attached schedules for a reconciliation of adjusted OIBDA to operating income (loss) calculated in accordance with GAAP for Liberty Interactive Group and Liberty Digital Commerce Group (Schedule 2). |

|

|

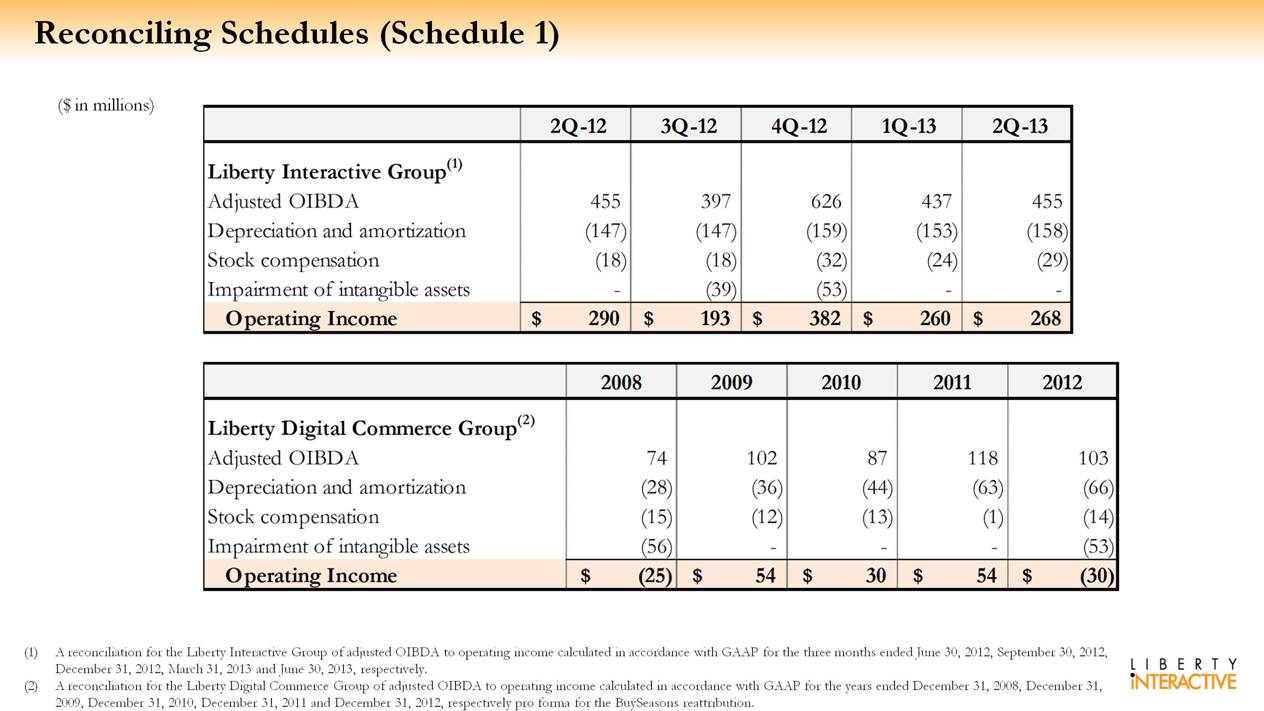

Reconciling Schedules (Schedule 1) A reconciliation for the Liberty Interactive Group of adjusted OIBDA to operating income calculated in accordance with GAAP for the three months ended June 30, 2012, September 30, 2012, December 31, 2012, March 31, 2013 and June 30, 2013, respectively. A reconciliation for the Liberty Digital Commerce Group of adjusted OIBDA to operating income calculated in accordance with GAAP for the years ended December 31, 2008, December 31, 2009, December 31, 2010, December 31, 2011 and December 31, 2012, respectively pro forma for the BuySeasons reattribution. ($ in millions) Liberty Digital Commerce Group(2) Liberty Interactive Group(1) 2Q-12 3Q-12 4Q-12 1Q-13 2Q-13 Liberty Interactive Group(1) Adjusted OIBDA 455 397 626 437 455 Depreciation and amortization (147) (147) (159) (153) (158) Stock compensation (18) (18) (32) (24) (29) Impairment of intangible assets - (39) (53) - - Operating Income $ 290 $ 193 $ 382 $ 260 $ 268 2008 2009 2010 2011 2012 Liberty Digital Commerce Group(2) Adjusted OIBDA 74 102 87 118 103 Depreciation and amortization (28) (36) (44) (63) (66) Stock compensation (15) (12) (13) (1) (14) Impairment of intangible assets (56) - - - (53) Operating Income $ (25) $ 54 $ 30 $ 54 $ (30) |

*****

Forward Looking Statements

The foregoing transcript and slides include certain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements about the proposed new tracking stock and other matters that are not historical facts. These forward-looking statements involve many risks and uncertainties that could cause actual results to differ materially from those expressed or implied by such statements, including, without limitation, the satisfaction of conditions to the proposed new tracking stock. These forward looking statements speak only as of the date of the communication, and Liberty expressly disclaims any obligation or undertaking to disseminate any updates or revisions to any forward-looking statement contained herein to reflect any change in Liberty’s expectations with regard thereto or any change in events, conditions or circumstances on which any such statement is based. Please refer to the publicly filed documents of Liberty, including the most recent Form 10-K and Forms 10-Q, for additional information about Liberty and about the risks and uncertainties related to Liberty’s business which may affect the statements made in the transcript and slides.

Additional Information

Nothing in the transcript or slides shall constitute a solicitation to buy or an offer to sell shares of Liberty Interactive’s proposed new tracking stock or Liberty Interactive’s existing common stock. The offer and sale of shares of the proposed tracking stock will only be made pursuant to an effective registration statement. Liberty Interactive stockholders and other investors are urged to read the registration statement to be filed with the SEC, including the proxy statement/prospectus to be contained therein, because they will contain important information about the issuance of shares of the proposed tracking stock. Copies of Liberty Interactive’s SEC filings are available free of charge at the SEC’s website (http://www.sec.gov). Copies of the filings together with the materials incorporated by reference therein will also be available, without charge, by directing a request to Liberty Interactive Corporation, 12300 Liberty Boulevard, Englewood, Colorado 80112, Attention: Investor Relations, Telephone: (720) 875-5408.

Participants in a Solicitation

The directors and executive officers of Liberty Interactive and other persons may be deemed to be participants in the solicitation of proxies in respect of proposals relating to the approval of the issuance of the new tracking stock. Information regarding the directors and executive officers of Liberty Interactive and other participants in the proxy solicitation and a description of their respective direct and indirect interests, by security holdings or otherwise, will be available in the proxy materials to be filed with the SEC.